Auto Insurance in New York

Car insurance in New York is an insurance product that safeguards the insured against monetary losses in the event of a car incident or vehicle theft. New York car insurance covers the damages to an insured’s car and protects them from liability for the losses, injury, or property damage sustained by others. Auto insurance has a variety of coverages you can choose from depending on what you need. You must purchase an auto insurance policy from an auto insurance company licensed to operate in New York and pay the required premiums to have auto coverage.

The Department of Financial Services is the agency responsible for regulating car insurance in New York. New York car owners are required to obtain the state minimum coverage car insurance (liability) before registering their vehicles.

Why Do we Need Auto Insurance?

New York drivers must purchase car insurance before registering their vehicles, and if they fail to do so, they risk suspension of their vehicle registration according to the New York financial responsibility law. Car insurance in New York protects car owners against financial loss arising from covered damages in an accident to their vehicle or a third party’s vehicle, legal fees, or medical expenses of an injured third party. Without car insurance, car owners would most likely have to bear these losses out of their pockets. Lenders may also insist car owners buy car insurance if they are financing or leasing their car. Car insurance aids in safeguarding lenders' or leasing agents' investment because they hold the lien on the cars while the car owners make payments. If a vehicle is damaged due to a covered loss, Car insurance will help pay for the necessary repairs or replacements. The leading cause of injury-related deaths in the State of New York is car accidents.

According to a motor vehicle traffic injuries report, the annual average of deaths and emergency State Department of Health visits between 2012 and 2014 in New York was 1,098 and 136,913, respectively. In the same period, there were 12,093 hospitalizations.

As reported by the Institute for Traffic Safety Management and Research (ITSMR), between 2018 and 2022, there were over 1.7 million crashes across the State of New York, with at least 4,190 of them fatal. In 72.07% of crashes, there was reportable property damage, while in 27.62% somebody got hurt.

| Crash Statistics in the State of New York

(based on data for 2018-2022) |

|

| Total Crashes | Average of 400,000 crashes annually |

| Property Damage | ≈ 285,000 damaged property per year |

| Personal Injury | Average of 110,000 people injured every year |

| Fatal Crashes | 881 - 1,061 per year |

New Yorker drivers need Car insurance to cover potential financial losses due to vehicle traffic crashes. Speak to a licensed auto insurance agent before you purchase New York car insurance coverage in New York. These agents have the knowledge and expertise to find affordable car insurance that suits your needs.

How Does Auto Insurance Work in New York?

Auto insurance in New York works in different ways depending on the type of coverage you have. Generally, auto insurance financially protects you from liability for another person's injuries or property losses and covers damage to your vehicle. If you or your passengers are hurt in an accident or hit by an underinsured or uninsured motorist, your auto insurance may also cover your medical expenses.

When applying for auto insurance coverage, the insurer will evaluate how much of a risk it is to insure your vehicle and set your premiums accordingly. Many factors may affect the cost of your insurance coverage, including:

Age

Gender

Location

The type of vehicle

Auto insurance premiums in New York can either be paid upfront or in installments (monthly or quarterly). Once your auto insurance application has been accepted, it is your responsibility to be consistent with premium payments to prevent your car insurance policy from lapsing. If an insured loss occurs, contact your insurance provider as soon as possible. Your insurer will appoint a claims adjuster, whose responsibility it is to evaluate the level of damage and calculate how much to pay you in accordance with your policy. You can contest the amount if you disagree with the adjuster's estimates. An auto insurer will likely raise premium rates during the term following the incident unless the policy offers an accident forgiveness feature. Consult with a licensed auto insurance agent to further understand how auto insurance works in New York. They can also help to get you affordable car insurance quotes that fit your insurance budget.

How Does Car Insurance Work If I am Not at Fault?

New York is a no-fault state. In no-fault states, each driver involved in an accident must file their auto insurance claims with their own car insurance companies, regardless of who was at fault.

New York drivers are required by state law to carry Personal Injury Protection (PIP) coverage with a minimum limit of $50,000 as part of their auto insurance policy. PIP coverage helps pay for your and your passengers’ medical expenses, including health insurance deductibles, lost wages, essential services you can’t perform due to accident-related injuries, and even funeral costs. PIP differs from Bodily Injury (BI) liability coverage—while PIP covers injuries to you and your passengers regardless of fault, BI covers legal expenses if someone sues you after an accident you caused.

When filing a no-fault claim in New York, you must do so through the insurance company covering the vehicle you were operating. If you were a pedestrian and were struck by a vehicle, you should file your claim with the insurer of the vehicle that hit you. In a hit and run situation where the vehicle cannot be identified, file your no-fault claim with the insurance company of a household family member, if available. If no household member has a policy, then you may turn to the Motor Vehicle Accident Indemnification Corporation (MVAIC). Claims must be submitted within 30 days of the accident.

Documenting as much information as possible at the scene is crucial, especially in hit and run cases. If you manage to note the license plate number of the fleeing vehicle, using a license plate lookup tool may provide valuable information that helps identify the responsible party. This can be instrumental if the at-fault driver attempts to avoid liability.

New York Auto Insurance Market

In 2019, 4.1% of drivers in New York were uninsured. Following this trend, currently there are around 500,000 uninsured drivers on our roads.

Per the New York financial responsibility law, the state minimum coverage is required for any vehicle with registered plates:

Minimum Coverage Car Insurance in New York |

|

| Bodily Injury Liability | $25,000 per person |

| $50,000 per incident | |

| Death Liability | $50,000 for death of person |

| $100,000 for death of 2 or more people | |

| Property Damage Liability | $10,000 per incident |

This means the insured would receive coverage up to $50,000 for all persons injured in an accident, subject to a limit of $25,000 per each individual, and $10,000 coverage for property damage. If someone dies in the accident, the policy will pay a minimum of $50,000 per death.

In 2021, New York ranked 4th in terms of property & casualty (P&C) premiums written, with more than $50 billion. Car insurance companies accounted for approximately 34% of that.

| PRIVATE AUTO INSURANCE in NEW YORK | |

| Type of Auto Coverage | % of all P&C insurance in NY |

| - Liability | 18% |

| - Collision + Comprehensive | 10% |

In New York, private car insurance companies collected over $14 billion in direct premiums. Auto liability accounted for nearly $9 billion of these, and collision and comprehensive was written for more than $5 billion. Direct premiums written for commercial auto insurance exceeded $2 billion. Auto liability was written for over $2 billion of these, and collision and comprehensive was written for about $420 million.

How Much is Auto Insurance for a Month?

The cost of full coverage car insurance in New York is around $3,000 annually or $250 per month. Auto liability insurance coverage typically costs between $85 and $1000 a month. Once you add comprehensive, collision, and uninsured driver coverages, the premium usually surpasses $1,500 per every 6 months of coverage.

The cost of your car insurance policy per month depends on factors such as age, gender, credit score, location, kind of vehicle, and the coverage limit. For instance, an individual may be offered cheaper car insurance rates because of their higher credit score, while someone with a poor or damaged credit history may pay higher rates for their car insurance coverage. You can take advantage of the mentioned factors to get the cheapest insurance rates possible.

The cost of your auto insurance can also be affected by your age. Generally, older drivers are less likely to be in accidents than inexperienced drivers, especially the young ones. Teen drivers and other young New York drivers under the age of 25 typically offered higher auto insurance rates. Teen drivers between the ages of 16 and 17 may have to spend over $500 to $600 per month for a car insurance policy. Adults, on the other hand, spend an estimated $150 to $170 in their 20s and $90 to $120 in their 50s (depending on the vehicle).

Your driving history can also affect the cost of your monthly car insurance premium. For instance, if you are an inattentive driver and it affects your driving record, the cost of your auto insurance policy would most likely go up. However, you can check your driving history kept on file by the New York Department of Motor Vehicles (DMV) to discover how many traffic violations and points you have. If you have points on your driving record, you can take action by contesting the ticket, enrolling in the state-approved traffic school, or making prompt payment of all fines. All of this would help in reducing the cost of your monthly car insurance premium.

The last and usually the main parameter that determines the cost of auto insurance coverage is the underlying value of the insured vehicle. In 2019, the average cost of a new car in New York was around $37,000. Meanwhile, in 2022, exacerbated by the supply shortage, the average cost of even pre-owned vehicles in the State of New York has climbed to over $34,000.

Consult with a New York-licensed insurance agent who is skilled to understand your needs and can match you with the most cost-effective option that meets your unique needs. The agent can also help you to better understand how various factors affect the cost of auto insurance in New York.

Why Does my Car Insurance Keep Going Up Without Filing Claims?

The main culprit of the increasing car insurance premium in the state of New York is inflation. Besides the economic factors, your insurance may go up if:

The amount of claims in your area has increased. In this case the insurer adjusts the rates based on a higher level of risk. If the risk goes up, the premium offered in that area must be high enough, so that the insurer can meet all of the claims that may originate from this area. Even if you change the address in the same city, you will likely see a change in the annual premium rate.

Traffic violations and speeding tickets. Insurance companies keep an eye on your driving record. If there is a negative moving violation on your record, it likely affects your cost of insurance.

High risk drivers. If you add other people to your policy, their driving records will affect your insurance coverage cost.

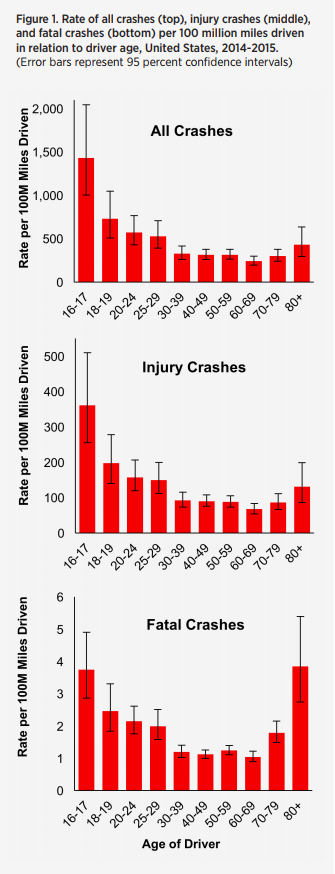

You are over 65 years old. While the insurance rates get cheaper with age, the opposite occurs when we get older than 60-65 years old. The rates start to go up, as we become potentially more dangerous and fragile behind the wheel. Past 80, a senior driver is as likely to get into a fatal crash, as they did when they were a teen driver. In 2022, there were over 3.2 million senior citizens in the State of New York.

{kind=link}

At What Age Does Car Insurance Go Down?

Drivers may expect 2 major drops in auto insurance coverage during their lifetime: at 25 and 35.

The first major lowering of costs happens in the span of 5 years, starting at 20 and ending at 25.

The second and usually last major drop in auto insurance coverage occurs over the course of 5 years: 30-35 years old.

Past 35, the premium adjusts mainly based on the changes in coverages, driving record, and the value of the insured vehicle - until you age beyond 60. At this point the premiums start going back up.

To find cheap coverage, discuss your auto insurance needs with a knowledgeable New York-licensed insurance agent with access to multiple companies.

Request an Auto Insurance Quote

QUOTE ME

What Types of Auto Insurance are in New York?

The main types of car insurance in New York are:

- Private auto insurance

- Commercial auto insurance

| AUTO INSURANCE in NEW YORK | |

| Type of Auto Coverage | % of all P&C insurance in NY |

| PRIVATE AUTO | 28% |

| COMMERCIAL AUTO | 6% |

Private auto insurance provides coverage for individuals and their privately owned cars. It also protects any person listed as a driver on another person's private motor insurance policy. The driver of a car is protected by private auto insurance when it is used for social, domestic, and other personal activities. Private auto insurance providers will provide coverage for your commute to and from work, but not to perform work - using the vehicle.

| Common types of private auto insurance available in New York | |

| Auto liability insurance | covers bodily injury and property damage caused to another driver and other occupants after an accident (required) |

| Comprehensive insurance | covers damage to your car caused by theft, vandalism, fire, floods, falling objects such as trees, and other natural disasters |

| Collision insurance | covers the repair or replacement costs of a damaged vehicle due to collision with another car or an object |

| Uninsured auto insurance | covers damage caused by an uninsured driver after an accident (required) |

| Underinsured auto insurance | covers the gap in the coverage of an underinsured driver after an accident |

| Personal Injury Protection (PIP) auto insurance | covers the insured driver's medical bills, lost wages, and other incidental expenditures after they are injured in an accident that results in bodily harm, regardless of who was at fault |

Be aware that you cannot conduct any commercial activity that involves business transactions using private auto insurance. You must insure your vehicle with a commercial auto insurance policy if you use it to further the operations of your business.

Commercial auto insurance in New York provides coverage for a vehicle used in the regular operation of a business, such as the one used to transport goods or passengers for commercial purposes. It covers liabilities that private auto insurance normally does not cover. Commercial auto insurance will cover company automobiles, trucks, and fleets of commercial vehicles, including those leased by business owners. It shares common auto insurance policy coverages like liability, collision, comprehensive, medical payments, and uninsured motorist coverage with private auto insurance.

Commercial and personal auto insurance share similar coverages and functions and the differences are determined by where you get them. The majority of private auto insurance providers do not offer commercial coverage. You can purchase commercial auto insurance coverage from New York-licensed insurance brokers and agents who specialize in Commercial Coverage.

Below are common auto insurance coverages in New York:

PROPERTY DAMAGE (PD)

Property damage liability auto insurance in New York protects you from financial loss arising from the replacement or repair costs for damage done to another person's vehicle or property in an accident for which you were liable. So, if you crash into your neighbor's fence and damage it, property damage liability coverage will pay for it. An average of 285 thousand property damage claims are made in New York every year.

Generally, property damage liability insurance does not apply to damages to your vehicle. You need to get other coverages for that, such as collision insurance.

What Does Property Damage Liability Auto Insurance Cover?

Property damage liability auto insurance in New York can cover the following:

- Damages to other people’s vehicles

- Damage to a third party’s property such as the house, mailbox, or fence

- Legal expenses incurred as a result of liability lawsuits filed against you for property damage

- Lost business income or wages caused by property damage

The following auto insurance policies can provide coverage for third-party’s property damage in New York:

- Liability coverage: The New York State Department of Motor Vehicles mandates the purchase of liability coverage before car owners can register their vehicles with the department. New Yorkers are required to show their ability to pay for the property damages and personal injuries caused by them in car accidents. They must maintain property damage (PD) liability coverage of at least $10,000 per accident.

Typically, your liability coverage will most likely cover the repairs and replacement of the other vehicle you may have damaged in an accident. However, since New York is a no-fault state, drivers would need to file auto liability claims with their insurance provider. However, if their coverage is not enough to cover their losses, they can sue the driver at fault as long as they meet the serious injury threshold provided for in Article 51 of the New York Insurance Law. The most commonly purchased coverage limit for property damage liability insurance is $100,000 per accident - Comprehensive coverage: This covers you when your car is damaged by incidents such as vandalism, natural disasters, theft, and riots. Purchasing comprehensive coverage is a cost-efficient way of covering your vehicle against non-collision risks. Although it is an optional coverage, you may be required to purchase it if you lease or finance your vehicle. The limit of your coverage will be determined by the actual value of your car. For instance, if your car is vandalized, your vehicle will be replaced at a depreciated value at the time it was vandalized, excluding deductibles

- Collision Coverage: New York collision auto insurance coverage helps cover your vehicle after an accident or collision with an object and pays for vehicle repairs or replacement. Even when the driver is not at fault, collision coverage is beneficial. Although it is not required in New York, people get collision insurance to ensure they have extra coverage. However, a driver can be obliged to get collision insurance if a vehicle is leased or financed by a lender. The real cash worth of your car is what the car insurance company pays out when you file a claim under collision auto insurance, as there is no coverage cap

- Uninsured Coverage: This covers property damage when involved in an accident with someone who does not have auto insurance or a hit-and-run driver. It covers repairs and replacements for vehicle damage brought on by an uninsured motorist who was at fault. Family members, passengers, and anybody else eligible for coverage under your policy are also protected by underinsured coverage. New Yorker residents are mandated to include uninsured coverage in their auto liability policy with minimum coverage limits of $25,000/50,000

- Underinsured Coverage: This protects an insured driver when the at-fault driver's liability insurance is insufficient to pay the costs of repairing or replacing damaged property. An underinsured motorist policy fills in the gaps left by the at-fault driver's inadequate insurance. The remaining costs will be covered by your underinsured motorist policy if the at-fault driver carries less liability insurance than required and causes damage that exceeds their limited coverage

BODILY INJURY (BI) - Car Insurance in New York

In New York, bodily injury auto liability coverage in your car insurance policy pays for the related medical expenses when you are at fault in an accident that results in injuries to another driver or passenger. It is important to note that bodily injury liability coverage does not apply to injuries experienced by the driver who was at fault in the accident. Medical payment coverage, a type of auto insurance not included under motor liability insurance, covers bodily injuries caused by at-fault drivers. An average 110 thousand New York residents receive bodily injuries as a result of car crashes annually.

What Does Bodily Injury Liability Cover?

Bodily injury auto liability insurance coverage in New York covers the following:

- Medical expenses such as hospital bills, emergency medical services, and ongoing medical expenses after a car accident

- Legal fees due to civil liability lawsuits filed against you by the injured party. This includes the cost of hiring legal counsel and other court-related expenses

- The pain and suffering of the injured party. It can cover claims of emotional trauma or protracted suffering caused by accident

- Any loss of income suffered by the injured party due to the inability to work as a result of the accident you caused

- The cost of the funeral in the unpleasant event an individual does not survive the accident (Nearly 1 thousand New Yorkers die in car accidents every year)

The following auto insurance policies provide bodily injury liability coverage in New York:

- Auto liability insurance: This covers bodily injuries and property damage sustained by third parties due to an accident. New York drivers are required to carry bodily injury liability with a state minimum coverage car insurance amount of:

- $25,000 for bodily injury and $50,000 for death for a person involved in an accident

- $50,000 for bodily injury and $100,000 for death for two or more people in an accident

- Medical payment coverage: This is an optional auto insurance coverage that covers medical and funeral expenses after a car accident

- Personal Injury Protection (PIP) coverage: This insurance coverage is also known as no-fault insurance in New York. Drivers are required to purchase a minimum PIP coverage amount of $50,000 in New York. It covers the insured driver's medical bills, lost wages, and other incidental expenditures after they are hurt in an accident that results in bodily harm, regardless of who was at fault. Lost income or other medical benefits not covered by a health insurance policy in New York are also covered under PIP coverage.

You and any household members under this policy will be protected from financial losses caused by an injury sustained in car accidents anywhere in the United States, its regions and possessions, or Canada. - Uninsured Motorist Coverage: In New York, all auto liability policies issued to car owners must include uninsured coverage with a coverage limit of at least $25,000/$50,000. This is to protect occupants who sustain bodily injuries in an insured vehicle at the hands of an uninsured vehicle. Even though less than 5% of vehicles in the state are uninsured, this still leaves half a million uninsured cars on the roads.

- Underinsured Motorist Coverage: This kind of insurance coverage comes in when the driver who caused the accident does not have sufficient auto coverage to cover injuries sustained by the other party. Having this coverage is not mandatory in New York

LIABILITY - Car Insurance in New York

Auto liability insurance covers any property damage and physical harm you cause to another driver or their passengers in an accident where you are at fault. The costs of funerals, lost income, and pain and suffering may also be covered by this coverage. In New York, drivers are required, by law, to have liability insurance. Auto liability insurance does not cover the injuries you sustain in an at-fault accident.

The minimum amounts of auto liability coverage a driver must get in New York are:

- $10,000 for property damage for a single accident

- $25,000 for bodily injury and $50,000 for death for a person involved in an accident

- $50,000 for bodily injury and $100,000 for death for two or more people in an accident

You would be better off purchasing additional auto liability insurance coverage so that any cost beyond the minimum limit will not be paid out of pocket. Auto liability insurance is also applicable to commercial vehicles. For example, if you own a business where you use a vehicle to transport goods and equipment or run business errands, you would need to purchase general commercial liability coverage along with your commercial auto insurance.

Note: When it comes to personal injury, New York is a no-fault state, that is, you can decide to file an insurance claim with your auto insurance company and get compensation. However, if the injury you have sustained cannot be covered by your auto insurance company, you can sue the at-fault driver. In this instance, you would need to meet the serious injury threshold stipulated under Article 51 of the New York State Insurance Law. Per Article 51, a serious injury is one that causes death, fractures, disfigurement, or any injury that stops a person from performing day-to-day activities.

What is the Difference Between Private and Commercial Car Insurance?

While personal auto insurance and commercial auto insurance coverages in New York primarily serve similar purposes, there are a few distinguishable features between the two. These differences include what they cover, coverage limits, eligibility, definitions, and exclusions. Below are some differences between personal auto insurance and commercial auto insurance in New York:

- Private auto insurance provides coverage for vehicles used for personal purposes, while commercial auto insurance provides coverage for automobiles used primarily for commercial purposes

- Commercial auto insurance bears higher risks than private auto insurance considering the possibility of having commercial vehicles on the road more frequently than privately-owned vehicles.

- In the case of personal auto insurance, damages caused to a privately-owned vehicle while it is being towed are not covered unless a tow and labor coverage was purchased before the accident occurred. Damages to a commercial vehicle, while it is being towed, are covered under commercial auto insurance

- Due to higher exposure to risks, commercial auto insurance policies tend to have higher deductibles than private auto insurance policies.

- Commercial auto insurance covers any loss due to damage to an insured commercial vehicle. However, private auto insurance only covers losses or damages caused by riots, fire, theft, and certain natural disasters.

Consult with a New York-licensed auto insurance agent about your insurance needs so they can suggest the appropriate type of coverage. For instance, if you lease a vehicle for business purposes, it must be covered by commercial insurance typically offered by brokers specializing in that type of insurance.

What is Car Replacement Insurance?

Some insurance companies licensed in the State of New York offer optional coverage, which increases the amount of the payout if the insured vehicle is considered a total loss. The coverage may be referred to as:

- New car replacement insurance

- Car replacement assistance

The coverage guarantees that if the vehicle is totaled, the insured receives 15%-20% extra of the vehicle’s actual cash value, making a purchase of a new vehicle much easier.

How it works: If the insured vehicle with an actual cash value of $20,000, a $0 deductible, and a CRA 20% option, is totalled, the insured receives $24,000 from the insurance company: $20,000 x 120% = $24,000. If there was a deductible involved, it gets deducted before the payout.

Does Auto Insurance Cover the Driver or the Vehicle?

Auto insurance in New York covers the vehicle and not the driver. If a driver wishes to be personally covered by their auto insurance policy, they would need to purchase extra coverage such as Personal Injury Protection (PIP) coverage. If someone borrows your car with permission and gets into an accident in which they are at fault, your auto insurance can cover them. Such a person would be covered under what is called permissive use. Essentially, it will apply as though you were the one driving the car. If the loss is beyond your coverage limits, the liability coverage of the borrower may kick in to cover the remaining costs. Also, note that your PIP insurance coverage only covers you and not anyone else who has borrowed your car.

It is not in every case that your auto insurance only covers your car. There are certain instances when coverage will follow the driver. For instance, according to the New York Department of Financial Services, rental cars may be covered by your auto insurance. If you have a car accident with a rental vehicle, your liability insurance will pay for any damage or injuries caused by you as it would if you were driving your own car. Additionally, the rental car itself may be covered by the collision and comprehensive insurance provisions of your policy. To further understand how auto insurance works when driving a vehicle that does not belong to you, speak with a state-licensed auto insurance agent.

How Does Car Insurance Work When you Get Into an Accident?

Due to the fact that New York is a no-fault state, you are expected to file a claim with your auto insurance provider after being involved in an accident. However, if your auto insurance coverage is not enough to cover the injury or property damage you have suffered, you may sue the at-fault driver only if the injuries you have sustained meet the injury threshold. Article 51 of the New York Insurance Law provides for the serious injury threshold. It states that a serious injury is one that causes death, fractures, disfigurement, or any injury that stops a person from performing day-to-day activities.

Once an accident has occurred and has been duly reported, you are to file a no-fault insurance claim with your auto insurance provider. This claim must be filed within 30 days of the accident. Once filed, the insurance provider will assign an adjuster to the case to determine the extent and costs of all the damages. After determining the costs, the insurance provider will pay for property damage or bodily injury costs. To further understand how auto insurance works after you have gotten into an accident, consult with a state-licensed auto insurance agent.

How Much Auto Insurance Coverage Do I Need?

How much auto insurance coverage you need in New York depends on a number of things. For instance, in New York, drivers must have at least the minimum required auto liability insurance coverage of 25/50/10 before they can register their vehicles. However, it is recommended that you purchase above the minimum required coverage. This is so you can avoid paying any cost above the required minimum coverage limit out of pocket.

Typical Available Options of Auto Liability Coverage in New York |

|

| Accident Bodily Injury Liability

(Per Person/Per Accident) |

25,000 / 50,000 |

| 50,000 / 100,000 | |

| 100,000 / 200,000 | |

| 100,000 / 300,000 | |

| 300,000 / 500,000 | |

| 500,000 / 500,000 | |

| 500,000 / 1,000,000 | |

| 1,000,000 / 1,000,000 | |

| Death Liability | $50,000 for death of person |

| $100,000 for death of 2 or more people | |

| Property Damage Liability

(Per Occurrence) |

10,000 |

| 25,000 | |

| 50,000 | |

| 100,000 | |

| 300,000 | |

| 500,000 | |

You also need to consider the cost of your car. Was it bought with a car loan or do you own the car altogether? This information can help you determine how much auto insurance you need in New York. The need for extra coverage, such as comprehensive, collision, medical payments, personal injury protection, and uninsured and underinsured motorist coverage, in addition to the minimum auto liability coverage, will also influence the amount of auto insurance coverage you need.

Generally, you need the amount of auto insurance coverage to cover what you may lose if a lawsuit is filed against you. Contact a New-York licensed auto insurance agent who can use their experience to help you determine how much auto insurance coverage you need.

Does NY Auto Insurance Cover:

Does Car Insurance Cover Rental Cars?

Yes, rental cars are covered by auto insurance in New York. In addition to liability protection while driving, it offers financial protection against physical damage to the rented vehicle. For instance, your collision or comprehensive coverage will pay the repair or replacement costs if the rented vehicle was stolen or involved in an accident while you were driving it. Your auto liability insurance will pay for any damages you cause to another person's property or vehicle while driving a rented vehicle. Before renting a car, find out if your auto insurance policy covers rented vehicles by speaking with a licensed auto insurance agent in New York.

Can I Use my Insurance When Renting a Car?

Yes. You can use your New York car insurance when renting a car, so you may not need to purchase extra protection from the rental car company. However, personal car insurance will only cover a rental car used for personal travels. You should get commercial coverage if you want to rent the vehicle for business purposes. Speak with a New York-licensed auto insurance agent for more information on how your auto insurance policy can work with a rented car.

Does Car Insurance Cover Repairs?

If the damage to your car was caused by an accident or another covered catastrophe, including a fire or theft, your New York auto insurance will cover it. Your auto insurance policy does not cover normal maintenance brought on by deterioration or mechanical failure. If your automobile collides with another vehicle or an object like a tree or fence, your collision coverage will pay for the damages. If your vehicle rolls over in a single-car collision, it will also cover the cost of repairs. Your comprehensive insurance will pay for the repairs if your car sustains damage in a non-collision incident. Additionally, if you damage someone else's car, your auto liability insurance will pay for the repairs.

Does Car Insurance Cover Windshield Replacement?

Instances when auto insurance will cover damage to your windshield and replace it in New York, are:

- When the windshield is damaged by a covered natural disaster, such as hail, landslide, or a falling tree. Under these circumstances, the damage to your windshield will be covered by comprehensive coverage

- When your windshield is damaged after you hit an object such as a fence or pole or you hit another vehicle. In this case, your windshield repair will be covered by collision coverage

With a $0 deductible on either of the coverages, the windshield gets replaced for free.

Does Car Insurance Cover Engine Failure?

Generally, your auto insurance policy in New York will not cover damages to your engine. Your engine will not be covered if the issue is some mechanical malfunction. However, there are exceptions to this, for instance:

- If there is a special mechanical breakdown insurance coverage within your auto insurance policy

- The cause of damage to the engine can be traced back to a recent accident

- The warranty on your car covers the damage

Does Car Insurance Cover Theft of Personal Items?

No. Personal items like your laptop, briefcase or mobile phone stolen from your car are not covered by your New York auto insurance policy. However, if your car or its contents was stolen while it was not even on your property, your residential property insurance may cover any personal items in the car at the time of theft.

If you have further auto insurance questions, make sure to speak with a licensed and knowledgeable New York auto insurance agent.